European Central Bank policymakers are entering the June Governing Council period with inflation, energy volatility and borrowing costs pulling policy in different directions. The article's timing was anchored by April 17, 2026. A rate increase is being discussed because price pressures remain uncomfortable, but the decision is not isolated from growth risks across the eurozone. The debate reflects a familiar central-bank dilemma. Moving too slowly can allow inflation expectations to harden. Moving too aggressively can tighten financial conditions for households, companies and governments already carrying heavy debt loads. The eurozone makes that tradeoff especially difficult because member states do not share the same fiscal position. Energy markets remain the most unpredictable variable. Any shock tied to the Middle East, shipping routes or oil supply can move inflation forecasts before domestic demand has changed. That makes the ECB's job harder because headline inflation can rise for reasons interest rates do not directly control.

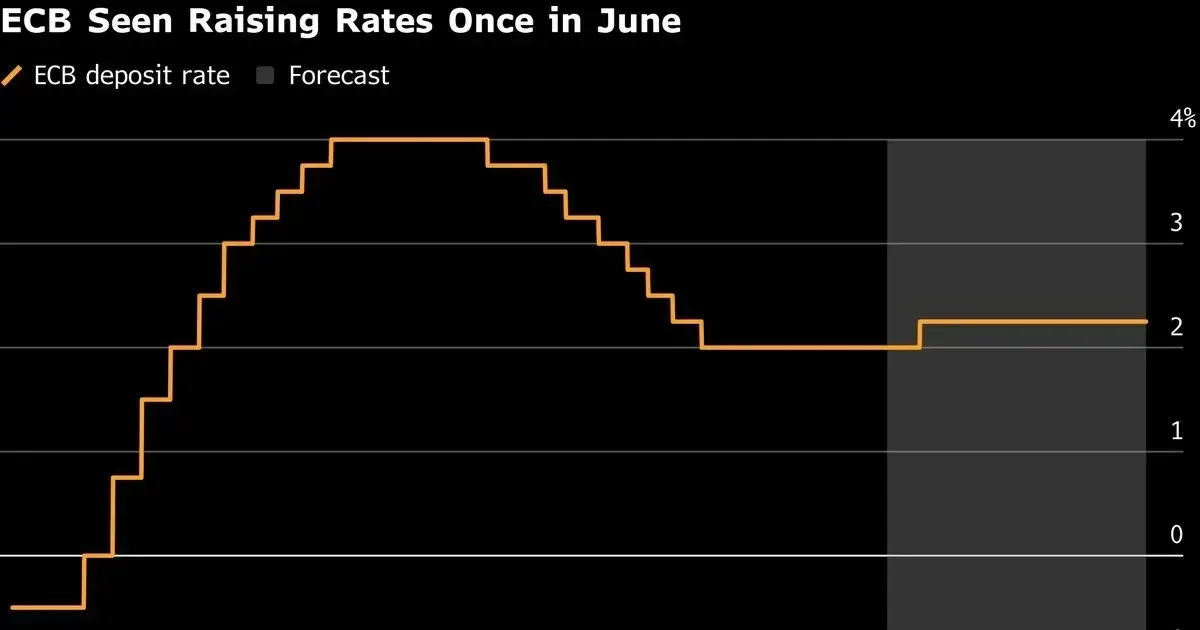

Inflation Pressure Keeps June in Focus

Economists watching the ECB have increasingly treated June as a live policy meeting. The central bank has to decide whether recent inflation pressure is temporary noise or evidence that the disinflation path has become less reliable. The answer will determine whether officials prioritize credibility or caution. A 25-basis-point increase would be the most conventional response if policymakers decide they need to reinforce their inflation target. It would signal that the ECB is still prepared to act even as growth slows. A hold would suggest officials believe existing policy is restrictive enough and that new shocks should be evaluated over more time. The communication may matter almost as much as the decision. Markets will parse whether the bank frames June as a one-off adjustment, the start of a renewed tightening cycle or a conditional move tied to incoming data.

Energy Costs Complicate the Eurozone Outlook

Higher oil and gas prices can raise transport, electricity and production costs across Europe. Those costs move quickly through headline inflation, but they do not always reflect stronger consumer demand. That distinction is central to the ECB's internal debate. If policymakers respond to every energy shock with higher rates, they risk suppressing growth while doing little to increase supply. If they ignore energy shocks, they risk allowing businesses and workers to build higher inflation into contracts. Neither option is clean. The eurozone's dependence on imported energy means geopolitical risk has a direct monetary-policy channel. Shipping disruptions, insurance costs and currency moves can all appear inside inflation data before households understand why prices changed.

Debt-Heavy States Face Higher Borrowing Risk

Rate increases affect member states unevenly. Countries with higher debt burdens feel rising yields more quickly, especially when investors begin demanding wider spreads over safer government bonds. That can revive concerns about fragmentation inside the currency union.

The ECB has tools designed to prevent disorderly market stress, but using them while tightening policy creates a delicate message. Officials want to fight inflation without appearing to finance governments. That balance has defined much of the eurozone's monetary history.

Bank lending also becomes more cautious as rates rise. Smaller companies, mortgage borrowers and developers are usually among the first to feel the effect. If credit tightens too sharply, the central bank could find itself fighting inflation while weakening investment.

Policy Guidance Will Shape Market Reaction

The June meeting will likely be judged by the guidance that follows. A rate hike paired with flexible language may calm markets more than a hold paired with hawkish warnings. Investors want to know whether the ECB sees inflation as a renewed trend or a volatile patch.

For households, the practical consequences are mortgage costs, savings rates and consumer prices. For governments, the consequences are budget interest bills and fiscal room. For companies, the consequences are financing costs and demand expectations.

The safest conclusion is that the ECB is not dealing with a simple inflation story. It is managing a shock-prone economy with uneven debt exposure and external energy risk. That makes June less about one rate decision than about how the bank explains its reaction function for the rest of the year.

Currency dynamics add another layer. A more hawkish ECB can support the euro, which may reduce some import-price pressure, but it can also tighten financial conditions for exporters. A weaker euro can lift imported energy costs even if domestic demand is cooling. Policymakers therefore have to read inflation through exchange rates, commodities and credit conditions at the same time.

The bank's credibility depends on explaining that complexity without sounding uncertain. Investors can accept conditional policy, but they punish confusion. June will show whether the ECB can keep optionality while still giving households, governments and markets a clear sense of its inflation priorities.

National central banks inside the Eurosystem will also influence expectations through speeches before the meeting. If officials sound divided, markets may test the edges of the ECB's message. If they converge around a narrow set of conditions, the June decision will be easier to absorb.